Line of Credit vs. Loan: Which is the Right Choice for You?

Navigating the world of personal and business finance can be complex, especially when you need to borrow funds. Two of the most common options you’ll encounter are a line of credit and a loan. While both provide access to capital, they function very differently. Making the right choice in the line of credit vs loan debate is crucial for your financial health. This guide will explore the fundamental difference between a line of credit and a loan, helping you determine which product is the perfect fit for your unique needs in 2026.

Key Takeaways:

- A loan provides a lump sum of money upfront, which you repay in fixed installments over a set period.

- A line of credit offers flexible access to a preset amount of funds, allowing you to borrow and repay as needed, much like a credit card.

- The primary differences lie in fund access, interest rates (typically fixed for loans, variable for lines of credit), and repayment structures.

- Your choice between a line of credit vs loan should align with your financial goal, whether it’s for a large, one-time purchase or managing ongoing, fluctuating expenses.

What Is a Line of Credit and How Does It Work?

A line of credit is a flexible financial tool that provides access to a predetermined amount of capital from a lender. Unlike a loan, you don’t receive the entire amount at once. Instead, you can draw funds from the account as needed, up to your credit limit. This makes it an ideal solution for ongoing projects, emergency funds, or managing unpredictable cash flow.

Understanding Revolving Credit

The core concept behind a line of credit is revolving credit. Think of it like a credit card: as you repay the amount you’ve borrowed, your available credit is replenished. For example, if you have a $20,000 line of credit and you withdraw $5,000, you have $15,000 remaining. If you then repay $3,000, your available credit increases to $18,000. This cycle of borrowing, repaying, and borrowing again can continue throughout the life of the credit line, offering significant financial flexibility. You only pay interest on the amount you’ve actually drawn, not on the total credit limit.

The Draw Period and Repayment Phase

Lines of credit typically operate in two distinct phases:

- The Draw Period: This is the timeframe during which you can actively borrow money from your credit line, usually lasting several years. During this period, your required payments might be low, often covering only the interest on the outstanding balance.

- The Repayment Phase: Once the draw period ends, you can no longer borrow funds. You then enter the repayment phase, where you must pay back the principal and any remaining interest over a set term, similar to a traditional loan.

What Is a Loan and How Does It Work?

A loan, often referred to as an installment loan or term loan, is a more traditional form of borrowing. When you’re approved for a loan, you receive the full amount of money in a single, upfront lump sum. This is a crucial point of distinction in the line of credit vs loan comparison. This structure is designed for large, specific purchases where you know the exact cost beforehand, such as buying a car, renovating a home, or consolidating debt.

Understanding Lump-Sum Installment Loans

With an installment loan, the terms are clear from the outset. You borrow a fixed amount of money and agree to pay it back over a specific period (the term). The repayment plan consists of regular, equal payments (usually monthly) that include both a portion of the principal amount and the interest accrued. Once the loan is fully paid off, the account is closed. If you need more funds in the future, you must go through the entire application process again.

Fixed Payments and Amortization

A key advantage of loans is predictability. Most personal and mortgage loans come with a fixed interest rate and a fixed repayment schedule. This process is known as amortization, where each payment is calculated to gradually pay down the debt. In the beginning, a larger portion of your payment goes toward interest. As time goes on, more of each payment is applied to the principal. This predictable structure makes budgeting straightforward, as you know exactly how much you owe each month and when the debt will be cleared.

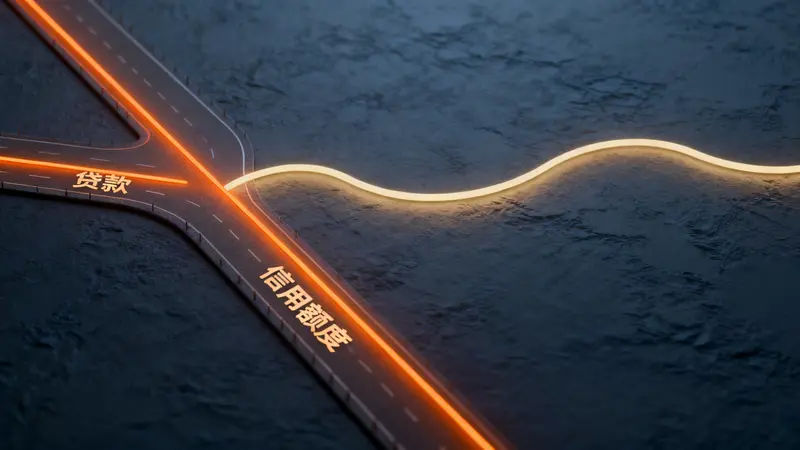

Key Differences: Line of Credit vs. Loan

Understanding the core distinctions between these two financial products is essential for making an informed decision. While both involve borrowing money, their structures are tailored for very different needs. The debate over a line of credit vs loan often comes down to a trade-off between flexibility and predictability.

Here’s a detailed breakdown of the key differences:

| Feature | Line of Credit | Loan |

|---|---|---|

| Access to Funds | Flexible, revolving access. Draw and repay funds as needed up to a credit limit. | One-time lump sum disbursed at the beginning of the term. |

| Interest Rates | Typically variable, tied to a benchmark rate like the prime rate. Your rate can change over time. For more on this, it’s useful to understand how interest rate fluctuations work. | Typically fixed for the entire term of the loan, providing predictable payments. |

| Repayment Structure | Flexible, often interest-only payments during the draw period. Principal is repaid during the repayment phase or can be paid down anytime. | Fixed, regular installments (principal + interest) over a set term until the balance is zero. |

| Best Use Cases | Ongoing projects with uncertain costs (e.g., home renovations), emergency funds, business cash flow management, overdraft protection. | Large, one-time purchases with a known price (e.g., buying a car, consolidating debt, funding a specific project). |

Pros and Cons of a Line of Credit

A line of credit offers unparalleled flexibility, but that freedom comes with its own set of responsibilities and potential risks. Weighing the personal loan vs line of credit pros and cons is a vital step.

✔ Advantages

- Financial Flexibility: Borrow only what you need, when you need it. This prevents you from taking on more debt than necessary.

- Interest Control: You only pay interest on the funds you use, potentially saving you a significant amount of money compared to a loan if you don’t use the full amount.

- Reusable Funding: Once you repay the borrowed amount, you can draw from it again without having to re-apply, making it a convenient source of ongoing capital.

- Emergency Preparedness: Having a line of credit open (even with a zero balance) can serve as an instant emergency fund.

✘ Disadvantages

- Risk of Overspending: The easy access to cash can tempt some individuals to borrow more than they can comfortably repay, treating it like a slush fund.

- Variable Interest Rates: If the benchmark rates rise, so will your interest payments, which can make budgeting difficult and increase the total cost of borrowing.

- Potential for Fees: Some lines of credit come with annual fees or inactivity fees if you don’t use them.

- Secured Requirement: Many of the largest and lowest-rate lines of credit, like a Home Equity Line of Credit (HELOC), require you to use an asset like your home as collateral.

Pros and Cons of a Loan

A loan provides structure and predictability, which is ideal for borrowers who prefer a clear path to becoming debt-free. However, this rigidity can also be a drawback.

✔ Advantages

- Predictable Payments: With a fixed interest rate and term, you know exactly what your monthly payment will be, making it easy to incorporate into your budget.

- Structured Budgeting: The lump-sum nature encourages disciplined spending, as you receive the exact amount needed for a specific purpose.

- Clear End Date: The amortization schedule shows a clear timeline for when you will be debt-free, which can be highly motivating.

- Often Unsecured: Many personal loans are unsecured, meaning you don’t have to put up collateral like your home or car.

✘ Disadvantages

- Less Flexibility: You receive the full amount upfront and start paying interest on it immediately, even if you don’t need all the funds right away.

- Re-application for New Funds: If you need more money, you must apply for an entirely new loan.

- Potentially Higher Total Interest: Because you are borrowing the full amount from day one, you may pay more in total interest compared to a line of credit where you only draw funds as needed.

- Prepayment Penalties: Some loans may charge a fee if you decide to pay off the debt ahead of schedule.

Recommended Reading

To make the best borrowing decision, it’s essential to understand the economic factors at play. Learn more about AI Stock Bubble or Market Correction? Positioning for the 2026 … to see how broader market trends can influence lending rates and product availability.

Qualification Requirements for Each

Lenders evaluate several factors to determine your creditworthiness for both a line of credit and a loan. While the core requirements are similar, there can be slight differences in emphasis. Generally, a strong financial profile will give you access to the best terms for either product. Exploring your options with a trusted financial platform like Ultima Markets can provide insight into managing your overall financial portfolio.

| Requirement | Line of Credit | Loan |

|---|---|---|

| Credit Score | Good to excellent credit (typically 670+) is required, as the revolving nature is seen as higher risk. | A wider range of credit scores may be accepted, but the best rates are reserved for those with good to excellent credit. |

| Proof of Income | Lenders need to see stable and sufficient income to ensure you can handle payments if you max out the line. | Stable income is crucial to show you can afford the fixed monthly payments. |

| Debt-to-Income (DTI) Ratio | Lenders prefer a low DTI ratio (ideally below 43%) to ensure you aren’t overleveraged. | A low DTI ratio is also critical, as the new loan payment will be added to your existing monthly debts. |

| Collateral | Unsecured options exist, but larger lines of credit (like HELOCs) require collateral (e.g., your home). | Personal loans are often unsecured. Auto loans and mortgages are, by definition, secured by the asset being purchased. |

Conclusion

The choice in the line of credit vs loan decision ultimately hinges on your specific financial needs and borrowing habits. There is no one-size-fits-all answer. If you need flexibility to manage fluctuating expenses or want an accessible safety net for emergencies, a line of credit is likely the superior option. Its pay-as-you-go structure can save you money if your borrowing needs are uncertain.

Conversely, if you are making a large, one-time purchase and value the stability of predictable payments for easy budgeting, a loan is the clear winner. Its fixed nature provides discipline and a definite end date to your debt. Before making a choice, carefully assess your project’s scope, your tolerance for variable rates, and your personal financial discipline. Ensuring the security of your finances is paramount, a principle highlighted by platforms focused on fund safety.

Frequently Asked Questions (FAQ)

1. When should I choose a line of credit over a personal loan?

A line of credit is ideal for situations with uncertain final costs or ongoing financial needs. Excellent use cases include home renovation projects where unexpected expenses can arise, a fund to cover emergency medical bills, or for a small business needing to manage irregular cash flow. If you value flexibility and only want to pay interest on the money you actually use, a line of credit is the better choice.

2. Is a HELOC (Home Equity Line of Credit) the same as a regular line of credit?

No, they are different. A HELOC is a specific type of line of credit that is secured by the equity in your home. This collateral typically allows for a much higher credit limit and a lower interest rate compared to an unsecured personal line of credit. However, it also carries the significant risk of losing your home if you fail to repay the debt.

3. Which has higher interest rates, a line of credit or a loan?

It depends. Unsecured personal loans often have higher starting interest rates than secured lines of credit like a HELOC. However, personal loans usually have a fixed rate, while lines of credit typically have a variable rate. This means that while a line of credit might start cheaper, its rate could rise over time, potentially making it more expensive than a fixed-rate loan in the long run.

4. Can I have both a line of credit and a loan at the same time?

Yes, absolutely. Many people use both products for different purposes. For instance, you might have a mortgage (a loan) for your house and a personal line of credit for emergencies or smaller projects. As long as your income and credit profile can support the debt, lenders will consider you for both.

5. What is the main disadvantage of a line of credit vs loan for debt consolidation?

For debt consolidation, the main disadvantage of a line of credit is the temptation to run up new debt. A loan gives you a fixed amount to pay off high-interest cards and then a structured plan to pay off that single loan. A line of credit, being revolving, allows you to borrow again after paying down the balance, which could undermine the goal of becoming debt-free if not managed with strict discipline.